Figuring out how to retire isn’t just about stacking cash – it’s about rethinking what retirement can actually look like. The answer isn’t just in saving more – it’s about designing your finances, habits, and lifestyle so that retirement becomes a reality on your terms.

Table of Contents

The Myths About Retirement (That Keep People Stuck)

A lot of what we believe about retirement isn’t true. In fact, some of the most common assumptions are exactly what leave people feeling stuck, unprepared, or disappointed when the time finally comes.

Myth #1: “I’ll figure it out when I get there”

Reality: Retirement is not a one-off decision, it’s a transition that can last 20-30 years. If you don’t plan ahead – financially mentally, and socially – you’ll be reacting instead of living intentionally. Start shaping the life you want before you leave work.

Myth #2: “Once I have enough money, everything else will fall into place”

Reality: Money is critical, but it’s not the whole picture. In big-cities like Singapore, you can retire with a strong bank balance but might feel lost without purpose, friends, or good health. Retirement readiness is a multi-legged journey, which we’ll dive into later.

Myth #3: “My partner and I will enjoy all this extra time together”

Reality: The adjustment is real. Retirement can strain relationships if one partner retires earlier or if both suddenly spend 24/7 side by side. Discuss expectations and carve out personal space before the shift happens.

Myth #4: “I’ll always want to stop working completely”

Reality: Many retirees discover they miss the structure, social contact, or intellectual stimulation of work. Partial retirement, consulting, or passion projects can provide income and meaning without the grind of a 9-to-9. It’s not weakness – it’s flexibility.

Myth #5: “I’ll finally have time to do what I love”

Reality: Free time doesn’t automatically translate into fulfilment. Without cultivating hobbies earlier, it’s easy to default to passive activities (like doom scrolling) that don’t bring satisfaction. Joy in retirement needs deliberate investment in yourself, not just time on the clock.

Why Retirement Mean Different Things to Different People?

After busting the myths, one truth stands out: retirement isn’t a single destination – it looks different for everyone. That’s why the first question to ask yourself isn’t “How much do I need” but rather “What does retirement even mean to me?”

For some, retirement is the ultimate escape: finally leaving the 9-to-5 grind, travelling, learning new skills, or just having the time to breathe. For others, they love what they do and want to keep going, but on their own terms. And then there are those who see retirement as a chance to flip the script – swapping their current job for something totally different.

Your why matters because it sets the scene for everything else. It shapes how much you need to save, how to plan your lifestyle, and even how you approach life outside of work. If we reduce retirement to just a number, we risk missing the bigger picture.

And that bigger picture comes down to four dimensions: your finances, relationships, mental well-being, and physical health. Nail these, and you’re far more likely to create a retirement that actually feels rewarding.

1. Financials – Know Your Number and Optimize

When it comes to planning how to retire, money is often the first thing people worry about. And it’s true – if you don’t get the numbers right, the rest of retirement can feel shaky. But financial planning isn’t just about chasing a big, magical lump sum.

It’s about understanding two simple drivers: income and expenses. Once you see the flow, you’ll know whether you’re on track or if there’s a gap to close.

Grab a piece of paper or open up Excel/Google Sheets. By the end, you’ll have your first version of a retirement plan.

Step 1: Define Your “Enough” for Retirement

Before you calculate anything, ask yourself: What kind of life do I want when I retire?

- Do you want to travel extensively? (you’ll likely travel way more in the early retirement years)

- Will you stay in your city but enjoy hobbies and dining out?

- Do you plan to support family or live solo?

Do this now:

- List your expected monthly costs in retirement: housing, food, transport, healthcare, hobbies, etc.

- Multiple by 12→ this give your annual lifestyle cost

Example (per month):

- Rent / housing: $2,500

- Food & groceries: $800

- Transport & utilities: $400

- Leisure/ travel: $1,000

- Misc/ healthcare/ contingency: $800

Total: $5,500/ month x 12 = $66,000/ year

Step 2: Calculate Your Income After Retirement

Focus on non-CPF (non-401k equivalent in U.S.) assets especially if you plan to retire early, because CPF is not available before age 55 (aged 59.5 for penalty-free withdrawal for 401k). Your CPF can still grow and serve as a safety net later, but it shouldn’t be counted in your early retirement cashflow.

Let’s look at:

- Passive income: Dividends, interest, rental income etc.

- Active income: For early retirees, ideally this is zero or minimal. If you plan semi-retirement or freelance work, factor this in

Example (non-CPF):

- Passive income: $12,000/year (from dividends/ interests/ rent)

- Side freelancing (if any): $10,000/year

Total: $22,000/year

Step 3: Map Your Retirement Gap

Compare your required annual expenses with your income sources. If you passive income + side freelancing fall short, that’s your “gap” you need to fill with additional savings or investments.

Example:

- Annual expenses: $66,000/year

- Passive income + side freelancing: $22,000/year

- Gap: $44,000/year → must come from portfolio drawdowns

The next step tells you how much your investment portfolio needs to be to close this gap.

Step 4: Project Your Portfolio Needed

Use a safe withdrawal rate (SWR) to estimate your target equity-investment portfolio. For early retirees, a common SWR is 3-4% to reduce the risk of running out of money.

Example:

- Annual gap: $44,000

- Withdrawal rate: 4%

- Portfolio needed: $44,000 ÷ 4% = $1.1M

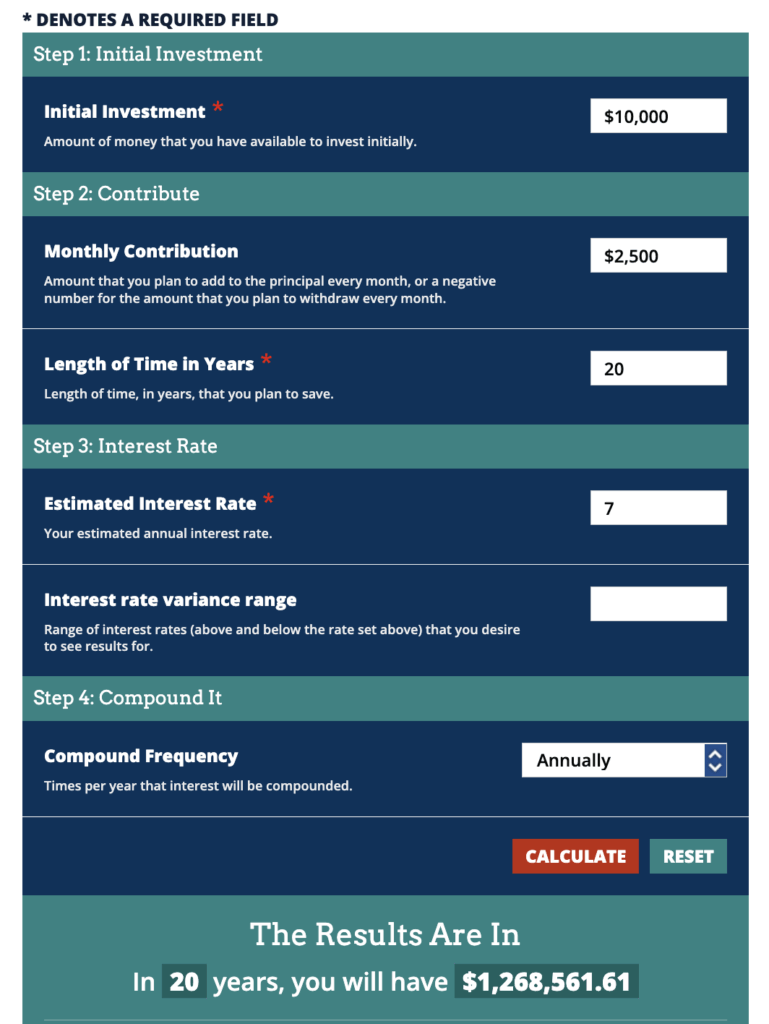

Don’t worry if you don’t already have the full portfolio amount today – that’s exactly where compounding comes in. Instead of stressing over the big number, let’s reverse-calculate what we need to do today.

Head over to any compound interest calculator and key in your own numbers:

- How much is your current stock portfolio?

- The number of years until your target retirement

- Your expected annual return (6-8% return per year for S&P 500 as an example)

You’ll see how small, consistent contributions can snowball into large amounts – even millions – over time. The goal here isn’t perfection, it’s progress: start with what you can, stay consistent, and let compounding do the heavy lifting.

Remember: This is the non-CPF portfolio target for early retirement.Your CPF can continue to grow in the background for later-life security, but it’s not counted in this number.

Step 5: Strategies to Close Your Portfolio Gap

Once you know your target portfolio size (Step 4) and your current savings, the next step is figuring out how to actually get there. Think of this as your roadmap – a mix of saving, investing, and optimizing resources.

1. Maximize Savings Rate (Sustainably)

- The faster you save today, the sooner your portfolio grows. Every extra dollar invested earlier has more time to compound

- Track your income and expenses, cut unnecessary spending, and direct that surplus towards investments

- Put any unexpected cash inflows (bonuses, salary increase from job promotion) into your portfolio

2. Invest Strategically

- Use a diversified mix of ETFs and stocks to grow your portfolio

- Focus on long-term compounding rather than short-term speculation

- For Singapore investors: consider funnelling excess cash to low-cost diversified ETFs for (like CSPX, QQQM) on low-cost platforms like IBKR/ Syfe Trade

3. Invest in Yourself

- In your 20-30s, you’ll likely have fewer commitments, less career lock-in, and more room to experiment. This is the time to switch roles, explore industries, or chase higher-paying opportunities that fast-track your earning potential

- Cutting expenses might save you a few hundred a month, but jumping from $3k to $5k in salary changes your entire retirement trajectory

3. Make CPF Work for You (Secondary Role)

While CPF can’t be touched until age 55-65 (depending on the account), it’s still a powerful part of your wealth-building strategy. Many people leave their CPF-OA balances idle at the default 2.5% interest, but you can put excess OA funds to work (funds above $20k that’s not being used for other purposes like housing)

For example, platforms like Endowus let you invest your CPF-OA into globally diversified, low-cost funds (like the Endowus exclusive Prime USA Fund). Instead of 2.5%, your CPF money could potentially grow at equity-level returns over decades – compounding in the background.

Think of CPF as your “later-life safety net”: while you rely on your own investments for early retirement, your CPF grows steadily in the background, helping you maintain security in your 60s and beyond.

Pro tip: While I recommend Endowus to invest excess CPF-OA, I wouldn’t use it for cash investing. For investing with cash, there are cheaper options like IBKR and Syfe Trade. If you want to try Endowus for CPF-OA investing you can use my referral link here – it gives you a fee rebate on sign-up!

2. Relationships – Preparing for the Shifts in Social Dynamics

People often underestimate how much retirement changes their social life. Don’t believe me? Think about how you feel when you take a long break from work. At first, it’s fun, – but soon you find yourself thinking about the office again – or missing the routine. Now imagine that “leave” never ends. That’s what retirement is: no work rhythm to anchor your days, no colleagues to banter with, no deadlines to grumble about together.

In fast-paced cities like Singapore, where our daily rhythm is defined by packed MRT rides, office lunches, and late-night WhatsApp work chats. Step away, and you may feel left out of the weekday buzz.

If you retire earlier than your peers, have you thought about who you’ll actually spend your days with? Most of your friends might still be working, leaving you with free time but little company. At home, dynamics shift too. If you retire before your partner, will you end up depending on them to fill your hours? If you both retire together, are you ready for what it’s really like to spend almost every waking hour under the same roof.

The city lifestyle makes this even more alarming. In smaller households, without the big extended families that were common a generation ago, your partner or a handful of close friends may be your entire social circle. Without preparation, retirement can quickly feel isolating.

So how can you prepare? Start by asking yourself:

- Do I have friendship and hobbies outside of work?

- Who will I spend time if my friends are still working?

- Have I thought about what everyday life with my partner will look like?

Don’t wait. Start building those connections now – nurture friendships, join communities, and talk with your partner about what “everyday life together” really looks like. Money funds retirement, but people make it meaningful.

3. Mental – Discover Yourself Beyond Your Career

Nowadays, much of our identity is tied to work – job titles, promotions, the next big project. But what happens when all that disappears? Many people only start thinking about hobbies or passions after retiring, when energy is lower and routines are harder to built. That’s why it pays to start now.

Don’t believe me? Think about weekends or long holidays – do you sometimes feel restless, like you’re not sure what to do with yourself without work? Retirement is that feeling, multiplied.

Ask yourself:

- If I stopped working tomorrow, what would get me out of bed with excitement?

- Do I have activities I’d enjoy even if no one else is around?

- Beyond career, who am I really?

“Filler” activities like doom scrolling social media or Netflix will never provide real satisfaction. What does is hobbies or activities that spark something in you – learning to paint, cooking new cuisines, picking up coding, joining a book club, or exploring mindfulness. The point isn’t about being “good” at something, but about building anchors you can rely on for purpose and joy.

The earlier you start, the smoother the transition. Retirement can be incredibly freeing if you already know what gives you energy. And in big cities, where keeping up can feel like a race, having a strong mental anchor makes sure you don’t lose yourself when the race is finally over.

4. Physical – Your Health is Non-Negotiable

With our busy lifestyles, it’s tempting to sacrifice health for hustle. Long hours, skipped workouts, late-night suppers – the trade-off feels harmless now. But here’s the irony: by the time you retire, the body you’ve built (or neglected) is one you’ll have to live with.

Think back to the last time you felt too tired after work to do anything but crash. Now imagine if that same lack of energy carried into retirement, when you finally have the free time you’ve been chasing. Free time means little if your body can’t keep up.

Ask yourself:

- Could I travel tomorrow without worrying about stamina or aches?

- Do I have the health to enjoy the hobbies I’m saving for later?

- Am I setting myself up for independence – or future medical bills?

Start now: move daily, eat better, sleep properly, and keep up with check-ups. These small investments pay off later in independence, mobility, and freedom – the things money can’t buy.

Conclusion

Retirement can feel daunting, but it isn’t just about money. It’s about designing a life you actually want – one supported by your finances, but also enriched by your health, relationships, and purpose.

Start small: define what retirement means to you, run your numbers, and take advantage of compounding early. Just as importantly, invest in your body, mind, and social ties so that your wealth has meaning when you finally step away from work.

Retirement isn’t the end – it’s the start of living life on your own terms. And if you plan it right, it’s the season where you finally get to live, laugh, lah – fully, freely, and without regrets.