An emergency fund is one of the most important foundations of personal finance – yet it’s also one of the most overlooked. Think of it as your financial safety net: money set aside to help you handle unexpected events like job loss, medical bills, or urgent repairs without falling into debt.

In this guide, we’ll break down exactly what an emergency fund is, why you need one, how much to save and the smartest places to keep it – so you can build peace of mind and stay financially ready at whatever life throws at you.

Table of Contents

What is an Emergency Fund?

An emergency fund is money you set aside for life’s surprises – the kind that throw your financial progress off track. Think of it as your financial shock absorber.

Instead of reaching for a credit card (and racking up interest) or borrowing from family, your emergency fund is there to catch you when:

- Your phone, laptop, or home appliance breaks down when you need it most

- A sudden medical bill pops up

- You lose your job and need time to find the next one (without stressing out too much!)

It’s not the same as your savings for travel, shopping, or a home downpayment. An emergency fund has one purpose only: to cover urgent, unexpected, and necessary expenses.

The best way to think about it? It’s like having an umbrella in your bag. Most days you won’t need it – but when the storm hits, you’ll be grateful it’s there.

Why You Need an Emergency Fund?

Life has a funny way of throwing curveballs when you least expect it. Without an emergency fund, even a small crisis can snowball into major financial stress. Here’s why having one matters:

1. Avoid Falling into Debt

When your car breaks down or a medical bill shows up, most people turn to credit cards. The problem? Credit card interest can hit 25% or more per year. An emergency fund protects you from being trapped in high-interest debt just to handle unexpected expenses.

2. Peace of Mind in Tough Times

Knowing you have money set aside means you don’t have to panic at every bump in the road. Instead of sleepless nights wondering how to pay the next bill, your emergency fund acts like a financial cushion that lets you breathe easier.

3. Freedom to Make Better Decisions

If you suddenly lose your job, having an emergency fund gives you the space to find the right next role – instead of jumping into the first job you can get just to pay the bills. That buffer can mean the difference between career growth and being stuck in something you regret.

4. Protecting Your Long-Term Goals

Without an emergency fund, you might be forced to sell your long-term investments at an unfavourable time (like during a market correction) just to cover urgent costs. That not only sets you back financially, but also disrupts your long-term wealth building plans. With an emergency fund in place, your investments can stay untouched and keep growing.

In short, an emergency fund isn’t just about money. It’s about control, security, and the freedom to handle life on your terms.

How Much Should Your Emergency Fund Be?

The short answer: most experts say 3-6 months of essential expenses. But in my opinion, it depends heavily on your lifestyle, job stability and household situation.

Step 1: Base it on Your “Bare-Bones” Lifestyle, Not Your Current Spending

When you lose your job, you’re not dining out every week, upgrading gadgets, or booking holidays. You’re in survival mode. That means your actual expenses will shrink.

So your emergency fund number should be based on your bare-bones budget – the absolute minimum needed to keep your life running:

- Rent or mortgage

- Utilities and groceries

- Transportation

- Insurance and medical costs

- Loan repayments

This number will almost always be less than your current monthly spending, because luxuries and “nice-to-haves” get cut during a crisis.

Step 2: Decide How Many Months to Save

Once you know your bare-bones monthly expenses, pick a runway based on income stability, household setup, and dependents:

- 3 months → Stable job, single, or living with family (no dependents)

- 6 months → Moderate job risk, mortgage/rent, or living with a partner and/or dependents

- 12 months → High-risk or variable income (freelance, volatile industry), single-income household, or situations where losing income would have the largest impact

For dual income households, you don’t need to double your fund. Base it on the higher-risk earner’s income, because the odds of both losing income at the same time are low (but not zero)

Step 3: Don’t Forget a Starter Cushion

Even before hitting your full target, having that initial $1,000-$2,000 saved makes a huge difference for smaller emergencies (medical bills, urgent repairs). From there, steadily build toward your full target.

Where to Keep Your Emergency Fund?

Once you’ve started saving, the next question is: where should you keep your emergency fund? The goal is to store it somewhere safe, accessible, and separate from your everyday spending money.

1. High-Interest Savings Account

Why it’s suitable:

- Safety: Deposits are insured up to $100,000 by the Singapore Deposit Insurance Corporation (SDIC)

- Liquidity: Easy access to funds with decent returns

- Simplicity: No complex requirements or lock-in periods

Top Picks:

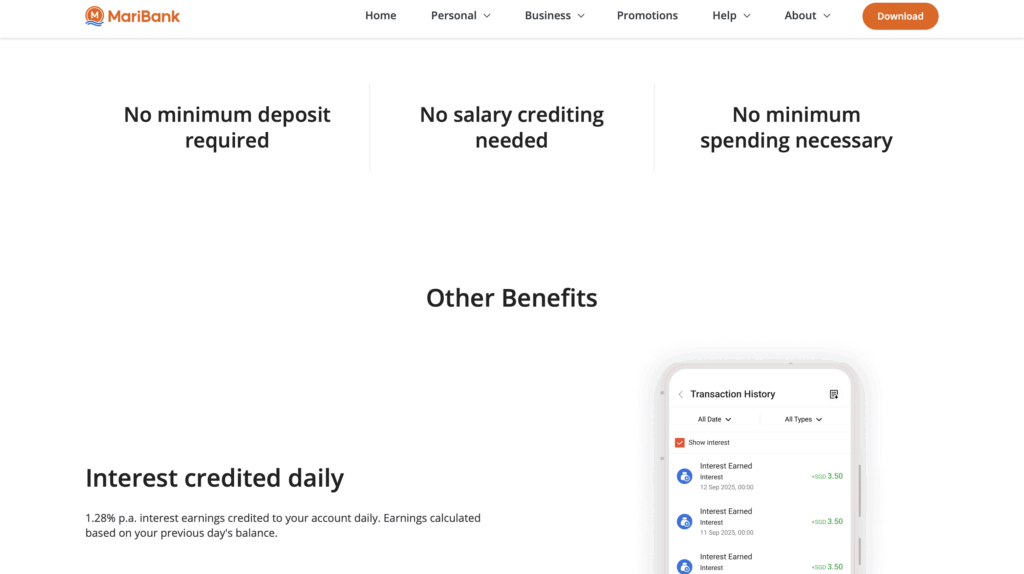

- MariBank Savings Account: Offers an interest rate of 1.28% p.a., with interest credited daily. No minimum daily, salary crediting or spending required (Referral code: 4XDM37IR)

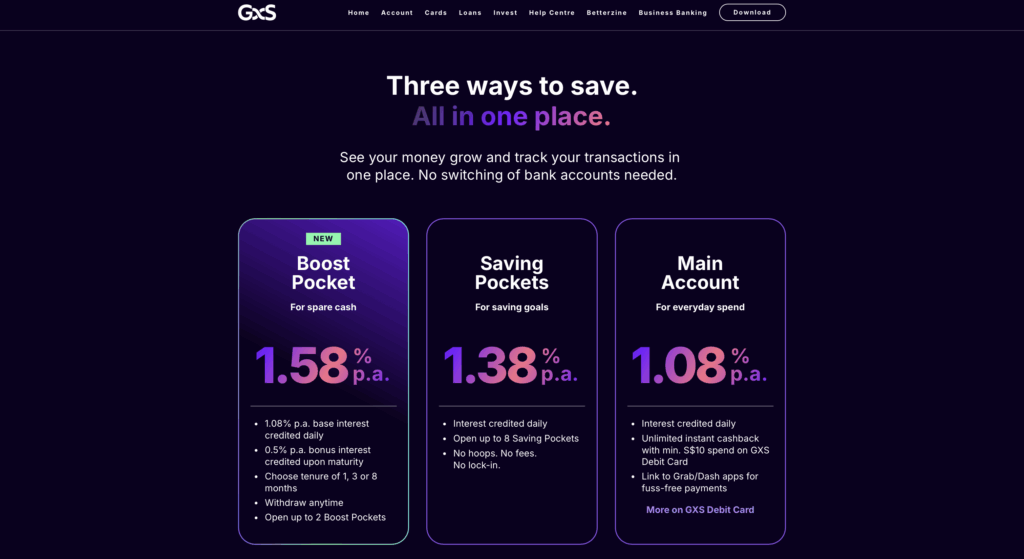

- GxS Bank (Savings Pocket): Provides an interest rate of 1.38% p.a., with interest credited daily. No minimum daily, salary crediting or spending required

Now, you might ask: Why not just use the UOB One or OCBC 360, since they advertise higher rates? The catch is most of those higher interest tiers require you to credit salary, spend on credit cards, or meet other requirements. If your emergency fund is around ~$10k (a common target), you may not qualify for the highest tier anyways.

Most importantly: keeping your emergency fund separate helps you avoid temptation of dipping into it. If it sits in the same account as your everyday spendable savings, it’s far too easy to blur the lines and treat it like “extra money”. This is coming from someone who has had a history of doing it, but you decide what’s best.

Note: Interest rates for these accounts can change over time. It’s advisable to monitor the rates periodically and consider switching between banks when it makes sense to maximize returns.

2. Fixed or Time Deposit (with flexible withdrawal preferred)

Why it’s suitable:

- Higher returns: Generally offer higher interest rates than regular savings accounts

- Safety: Deposits are insured up to $100,000 by the SDIC

Top Picks:

- MariBank Fixed Deposit: Offers fixed deposit tenures of 1, 3, or 6 months with an interest rate of 1.50% p.a.. Interest is credit upon maturity (Referral code: 4XDM37IR)

- GxS Bank (Boost Pocket): Provides fixed deposit tenures of 1, 3, or 8 months with an interest of 1.58% p.a.. Interest is credit upon maturity.

3. Money Market Funds

Why it’s suitable:

- Safety: Invests in a diversified portfolio of short-term, low-risk instruments

- Liquidity: Easy access to funds with competitive returns

- Returns: Generally offers higher returns than traditional savings accounts and fixed deposits

Top Pick:

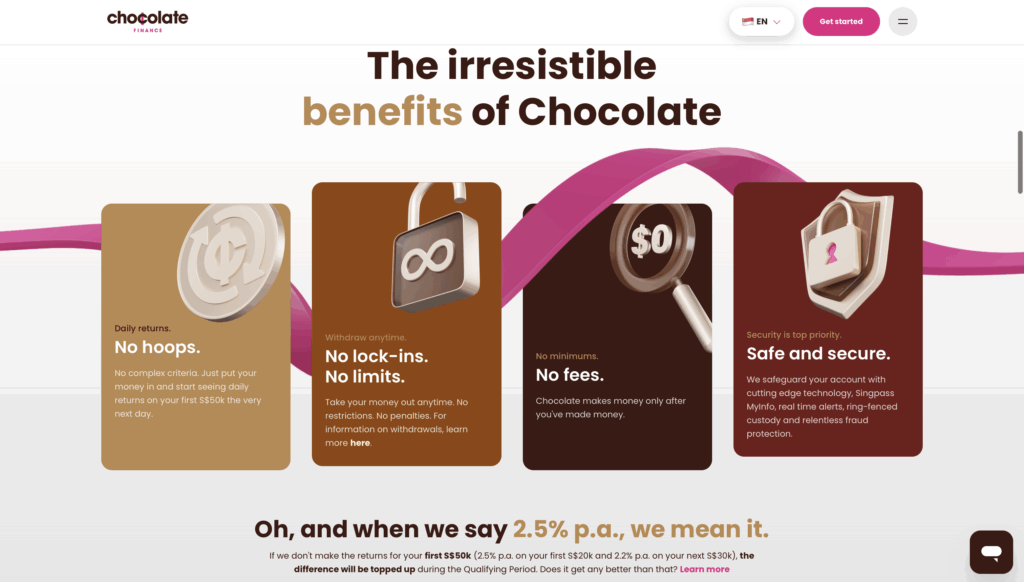

- Chocolate Finance: Offers returns of 3.0% p.a. on your first $20k, 2.7% p.a. on your next $30k, and up to 2.7% p.a. on any amount above that (Sign up here)

Note: These funds are low-risk but not risk-free. It’s essential to understand the underlying investments and associated risks before investing.

Common Mistakes with Emergency Funds

Even with the best intentions, many people slip up when building or managing their emergency fund. Here are the biggest pitfalls to avoid:

1. Treating Credit Cards as Emergency Fund

It’s tempting to think, “I can just swipe my credit card if something happens”. But here’s the problem:

- For one-off emergencies (like a $500 repair), your card works only if your next paycheck can cover it

- For bigger of longer-term emergencies (like job loss), a card without cash behind it quickly turns into high-interest debt

Think of it this way: your credit card is the tap, your emergency fund is the water tank. The tap let’s you spend instantly, but without cash in the tank, the tap runs dry

2. Keeping Too Much in Cash

Yes, cash is safe – but holding way more than you need means your money is just sitting idle. Beyond your emergency fund and short-term targeted savings (like a home downpayment, wedding fund, or near-term big purchase), extra cash should be working harder for you in investments.

Otherwise, you risk losing out to inflation while your money could have been growing.

3. Underestimating Your Needs

Many people only save for obvious bills (like rent or food), forgetting about:

- Medical emergencies

- Insurance deductibles

- Family support obligations (if any)

- Car or home repairs

An incomplete estimate leaves you underfunded when real life hits.

4. Locking It Up in the Wrong Place

Stocks, ETFs, or crypto might look tempting because they can earn higher returns. But the problem isn’t liquidity – it’s volatility. If an emergency strikes during a market downturn, you’ll be forced to sell at a loss, right when you can least afford it.

Emergency fund kept as cash under your pillow is not ideal too – as it’s easy to spend and not safe against theft, fire, or accidents.

The golden rule: Your emergency fund should be in stable, low-risk accounts (savings accounts, or money market funds), where the value is preserved regardless of market conditions.

5. Forgetting to Review and Adjust

Your expenses change over time – moving house, having kids, or switching jobs all affect your bare-bones budget. If your fund hasn’t grown with your life, it might not be enough when it matters most.

Conclusion

An emergency fund isn’t about big returns – it’s about peace of mind. It protects you from falling into debt, selling investments at a loss, or making desperate choices when life throws a curveball.

Start simple: know your bare-bones expenses, set a target (3, 6, or 12 months), and keep the money in safe, accessible places like high-interest savings account or money market funds.

Your emergency fund won’t make you rich, but it will keep you steady – and future you will be grateful you started.